When we hear about Wall Street billionaires, high-stakes trades, and massive financial moves, the conversation usually centers around one thing: hedge funds. But despite being frequently mentioned in the news, the actual mechanics of what these funds do remain a mystery to most everyday investors.

So, what exactly is a hedge fund, and how does it differ from a standard retirement account or mutual fund? Here is everything you need to know.

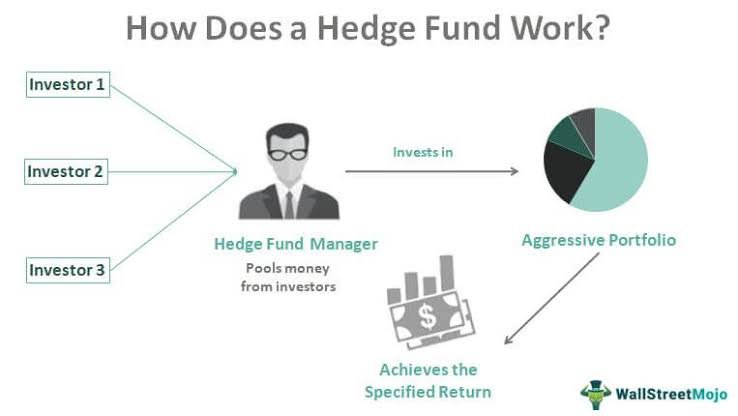

What is a Hedge Fund?

At its core, a hedge fund is a private, pooled investment vehicle. A fund manager gathers capital from a select group of wealthy individuals and institutional investors (like pension funds or university endowments) and invests that money across a variety of assets to generate high returns.

The word “hedge” originally referred to the financial practice of reducing risk. The first hedge funds, created in the 1950s, sought to “hedge” against market downturns by betting that certain stocks would go up (going long) while simultaneously betting that others would go down (short selling). Today, while many still use hedging techniques, the term broadly applies to funds that use aggressive, complex, and highly flexible investment strategies to beat the market.

Key Characteristics of a Hedge Fund

Unlike traditional mutual funds or Exchange-Traded Funds (ETFs) available to the general public, hedge funds operate under a unique set of rules:

- Accredited Investors Only: Because hedge funds are loosely regulated by government bodies like the SEC, they are legally restricted to “accredited investors.” This means you generally need a net worth of over $1 million (excluding your primary residence) or a significantly high annual income to participate.

- The “2 and 20” Fee Structure: Historically, hedge funds charge a standard “2 and 20” fee. The manager takes a 2% flat management fee on the total assets each year, plus a 20% performance fee on any profits generated.

- Use of Leverage and Shorting: Hedge funds are not limited to just buying stocks and holding them. They frequently use “leverage” (borrowing money to multiply their buying power) and short selling to profit even when markets crash.

- Illiquidity (Lock-Up Periods): If you put your money into a standard mutual fund, you can usually withdraw it the next day. Hedge funds often have “lock-up periods” lasting a year or more, meaning investors cannot access or cash out their money quickly.

Common Hedge Fund Strategies

There is no single way a hedge fund operates. Managers specialize in different strategies depending on their expertise and market conditions:

- Long/Short Equity: The most traditional strategy. The fund buys stocks it believes are undervalued and borrows/sells stocks it believes are overvalued. This balances the portfolio against broad market crashes.

- Global Macro: These funds focus on large-scale economic trends rather than individual companies. Managers analyze interest rates, inflation, currency shifts, and geopolitical events to make massive bets on entire countries or commodities.

- Event-Driven: These funds look for pricing inefficiencies caused by specific corporate events. They invest in companies going through mergers, acquisitions, bankruptcies, or major restructurings, aiming to profit from the temporary market confusion.

- Quantitative (Quant) Funds: Instead of human stock-pickers, these funds rely on complex mathematical models, high-frequency trading algorithms, and artificial intelligence to execute thousands of rapid trades based on statistical trends.

Hedge Funds vs. Mutual Funds

While both pool money from investors, their philosophies are entirely different. Mutual funds generally aim to track the market and provide steady, long-term growth for everyday retail investors. They are highly regulated, transparent, and charge low fees.

Hedge funds, on the other hand, aim for absolute returns. A hedge fund manager’s goal is to make a profit regardless of whether the stock market goes up or down. To achieve this, they take on significantly more risk, use complex financial derivatives, and operate with far less public transparency.